April '26: The Lookalike Spring

The March housing data looks good, and that might be the problem. Denver's spring is showing up pretty much the way spring is supposed to show up: buyers are back, homes are moving faster, and sellers are seeing real competition again for the first time in a year. Nationally, the jobs print came in stronger than expected, mortgage rates drifted back down from their war-driven highs, and the Iran ceasefire pulled some of the panic out of energy markets. Any reasonable read of the last thirty days would call this a recovery.

But the shape of this spring looks an awful lot like last spring, and last spring did not carry into the back half of the year. The question we keep coming back to is not whether March was real, because it clearly was, but whether the things underneath it can hold together into summer and fall. On that question, the signals are mixed at best, and tilted unfavorably at worst.

The Skim:

1. The Lookalike — Spring '26 rhymes with spring '25, but the backdrop is worse

2. Three Pipelines — Fertilizer, jet fuel, and consumer credit are already in motion

3. Denver — Qualified buyers are showing up and paying up, but the market is splitting

The Lookalike

Spring 2025 looked a lot like this one. Buyers came back after a slow winter, pendings firmed up, days on market dropped into the low teens, and prices ticked higher through June. And then, quietly, the whole thing faded. Pendings drifted lower through the summer, listings stretched out longer, and by January of this year Denver produced its slowest month in our dataset by a meaningful margin. It was not a collapse; it was a slow fade, and we tracked it in real time in the January and March pieces.

What is different this year is not the shape of the spring but the macro ground it is sitting on. Last year's fade happened while the Fed was cutting, inflation was drifting toward target, and mortgage rates were trending down. The economy was slowing with room to breathe. This year, the comparable setup is almost the inverse. CPI re-accelerated in March, the Fed has signaled it is on hold longer than markets wanted, consumer sentiment just posted the lowest reading in the history of the University of Michigan survey, and the ceasefire that brought rates down two weeks ago expires tomorrow with no meaningful progress on an extension.

Same spring, different foundation. The rest of this piece is about the differential.

The Three Pipelines

March's CPI print was mostly a gasoline story, and gasoline can unwind quickly if the Strait of Hormuz reopens and oil settles back toward the mid-seventies, which is roughly what the back end of the futures curve is pricing. That part of the inflation picture is recoverable.

The part that is not recoverable, at least not on a ceasefire headline, is three slower pipelines that are already in motion. These are not forecasts. They are mechanical consequences of decisions already made.

Pipeline One is fertilizer into food. A third of the world's seaborne fertilizer trade runs through the Strait of Hormuz, and prices for the major nitrogen inputs are up between thirty and fifty percent since February. A mid-April Farm Bureau survey found that roughly seven in ten American farmers cannot afford the fertilizer they need for the 2026 crop year. The choice they are making right now, at planting, determines yields in the fall. Consumer food inflation is projected to inflect in the May-to-August window, and the decisions driving it are already in the ground.

Pipeline Two is jet fuel into logistics. U.S. jet fuel prices roughly doubled in five weeks, Europe is running on a matter of weeks of remaining supply according to the IEA, and most major global carriers are already cutting capacity for the summer. The piece that matters for the domestic consumer is not actually airfare; it is diesel, which has moved in lockstep with jet fuel. Every truck carrying food to a grocery store is now carrying a materially higher fuel cost than it was two months ago, and that cost shows up on the shelf with a lag.

Pipeline Three is the consumer credit picture at the bottom of the distribution. This one started well before the war. Total household delinquencies are at their highest rate since 2017, subprime auto delinquency hit a record high in January, student loan serious delinquency is up an order of magnitude from a year ago, and mortgage delinquencies are climbing fastest in the lowest income quartile. The bottom of the consumer stack is already stressed, and it is about to get a food, fuel, and logistics shock layered on top of it.

None of this shows up in the top-line spending data yet, because the top twenty percent of households account for most discretionary spending and they are still mostly fine. But the transmission from bottom-quartile stress into broader consumption has historically taken three to six quarters, and the bottom clearly inflected last summer. That puts the likely arrival point somewhere in late 2026 or early 2027. It also puts it squarely in the window where we are asking whether this spring's housing momentum can carry into fall.

Denver: Demand is Back, but Split

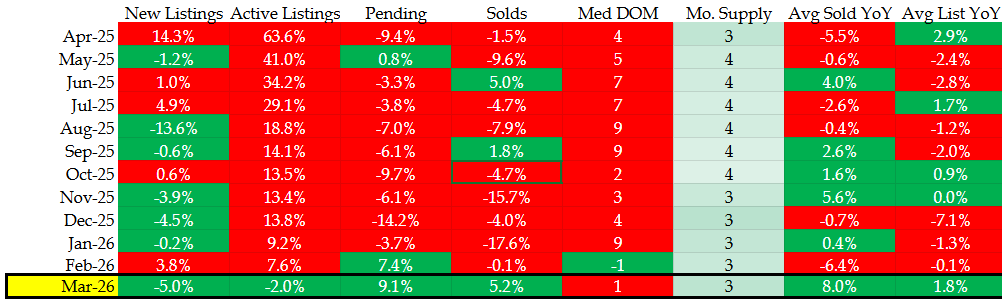

Let's check our trusty table summarizing the market conditions in the Denver metro area:

Denver Metro Real Estate Market Data - REColorado, April 2026.

Against that backdrop, Denver's March was genuinely strong, and it is worth saying clearly before we get to the nuance. New listings were down versus a year ago, pendings were up, closings were up, and days on market compressed back into the low teens. Supply is tight, buyers are competing, and the market is functioning the way a spring market should function.

The most interesting thing in the table is the relationship between list prices and sold prices. In March of last year, homes sold for roughly what they listed for on average. In March of this year, sold prices ran meaningfully above list prices, which is the cleanest signal we have seen in a year and a half that real buyer competition is back on well-priced inventory. Our read is that sellers came into March still anchored on the weak fall and frozen January, so they priced defensively, and the qualified buyers who showed up rewarded that pricing with aggressive bids.

The people showing up are the employed, qualified, move-up or move-laterally buyer who has been waiting for a window. The labor market has become unusually low-churn, which is not great if you are looking for a job but is stable if you already have one, and this buyer is finally deciding the math works at 6.30% rates. The people who are not showing up are the first-time buyer, the marginal buyer, and the buyer who is sensitive to every extra dollar of gas or groceries. Wage growth is at its weakest annual reading since 2021, real wages went negative in March, and consumer sentiment is telling you exactly how that cohort feels about writing a mortgage application right now.

The takeaway for anyone transacting in the next sixty days is that the spread between list and sold is unusually wide, which is the kind of thing that corrects. Sellers will see March's closings and price April and May listings higher. When they do, the asymmetric opportunity buyers have right now starts narrowing. It is real, it is now, and we do not think it carries deep into summer.

Denver: Supply, and the Two-Market Problem

The detached market is carrying the spring. Well-priced homes in good condition are moving quickly and often with multiple offers, and that is where the list-to-sold spread is being produced. If you are a detached seller with a clean home and a realistic price, the next two months are your window.

The attached market is where the macro thesis reaches Denver first. The rental data is the better signal right now, and it is pointing the wrong direction. Median rent is flat year over year, price per square foot is slightly down, and it is taking longer to lease a unit than it did a year ago. The luxury apartment glut we wrote about in March is still absorbing, and it is absorbing into a tenant base that is getting squeezed on everything outside of rent.

The core for-sale condo buyer is a first-time buyer, and that is the exact cohort feeling every one of the pipelines in the prior section. Their grocery bill matters. Their student loan matters. Their car payment matters. And their alternative to buying a condo, which is renting a newer building with a pool and a gym, is getting cheaper in real terms every month. The math to own keeps getting worse for this buyer even as the math to own a detached home keeps getting better for a different one.

If you are selling a condo, the comp set is wider than it looks. It is not just the other condos on your street. It is every luxury apartment that opened in the last three years, and it is competing for a buyer whose budget is already under pressure. Price it to move, because the buyer pool for attached product is getting smaller, not larger.

Looking Forward

The spring window is real, and if you are a qualified buyer who has been waiting for the right moment, the next sixty to ninety days are genuinely it. Supply is tight, sellers have not yet caught up to what March is telling them, and rates are the lowest they have been since the war started. That is a rare combination, and rare combinations tend to resolve.

The harder question is what happens on the other side of this window, and the honest answer is that the setup for the back half of this year is worse than the back half of last year was. Even if the ceasefire holds, the jet fuel shortage still lands in May, the food pipeline still lands in July, and the consumer credit picture at the bottom of the stack is still deteriorating. None of that is priced into the current housing data, because the current housing data is a spring market doing spring market things.

The single variable most worth watching for the rest of the year is not the Fed funds rate; it is the grocery bill. The April CPI print on May 12 is the first real read on whether the food pipeline is starting to land. The April jobs number on May 8 will tell us whether the low-hire, low-fire equilibrium is still holding. And the ship traffic through the Strait of Hormuz, rather than the ceasefire headlines, is what actually determines whether any of this improves.

For buyers, if you are qualified, the window is now. For detached sellers, price realistically and let the market reward you for it. For attached sellers, be honest about what you are competing with and price to move. For everyone, the advice from March still holds: do not trust anyone who tells you they know exactly how this ends.

We titled last month's piece "The Straw" because the camel's back was loaded and something was threatening to break it. The camel has not fallen. But it is still carrying everything it was carrying then, with a few new things on top, and the walk just got longer.