Dog Days

August 2025

With end-of-summer routines, back-to-school prep, and the FedEx Cup Playoffs in full swing, this is the time of year when people tune out both the economy and the real estate market for a few weeks. (And honestly, after such a busy year, we’ll take a quick breather ourselves.) Despite some major headline economic numbers over the last two months—and especially last week—the markets barely reacted. Meanwhile, the Denver real estate market continues to cool slightly, though without flashing any real warning signals. It’s what we expect during the dog days of August: squeezing in every last warm day before returning to work, grabbing a PSL, and flipping on college football.

The Skim:

1. Did You Just See That?

2. Demand: Flat

3. Supply: Leveling Off

Did You Just See That?

If you told a trader at the top of an economic cycle that in a single week core inflation surpassed expectations and ticked back above 3.0%, producer prices jumped nearly 1.0% month-over-month (driven largely by food costs), and retail sales came in weak, you’d expect a sharp market reaction. Instead, the response was muted. Taken together with last month’s disappointing jobs report, the chances of something brewing under the surface are rising.

The CPI and PPI data are worrisome for two key reasons:

1. Policy Pressure: The Federal Reserve is under intense pressure from the executive branch to cut rates and bolster the labor market. Inflation drifting further from the 2.0% target ties the Fed’s hands, reducing room to maneuver lower. This increases the likelihood that criticism of Chair Powell will grow louder. Recent reporting highlights that producer prices in July surged by the most in three years—something analysts partly attribute to tariff-related costs filtering through supply chains.

2. What’s Driving the Numbers: On the CPI side, one of the sharpest cost increases over the past year has been in medical care services (+4.3%). With Baby Boomers moving from salaries to fixed incomes, higher medical costs will eat away at their ability to spend and pass wealth on to younger generations. On the PPI side, July’s surge in food costs—driven by milk prices—adds to broader inflation pressure. And it’s not just about commodities: the agricultural sector is under strain from aggressive ICE raids and slowing immigration (legal and otherwise). A Cornell study suggests intensified raids in California alone have pushed producer prices up 7–12%, while farm labor shortages more broadly are driving double-digit wage increases in some regions. As farms face labor scarcities, those costs ripple outward into higher produce and protein prices. While not all of this will filter directly into consumer prices, it’s clear these structural factors are adding to the inflation picture.

For everyone outside the Baby Boomer cohort, higher food costs plus higher inflation reduce discretionary spending power for homes, entertainment, and beyond. We’ll keep watching consumer spending as a gauge of household health. With housing starts just reported at a five-month high, we’re hoping this late-summer data proves to be a blip rather than the beginning of a troubling trend. Still, recent surveys show that households are already shifting spending—cutting back on discretionary purchases as grocery and dining costs weigh heavier than they did a year ago.

(Quick Side Note on AI)

We haven’t touched on this much in recent letters, but we’re big believers in AI’s potential. Large language models and AI agents are already reshaping the workforce—and we expect the disruption to accelerate. This website you’re reading is a small example: in the past four months, we’ve built two proprietary tools, including Avery. This is the first public-facing real-estate-trained AI Agent (to our knowledge) who is operating as our brokerage's online receptionist -- and it's learning how to do more each day. Six months ago, this project would have required $300,000+ in development costs and nearly a year of production time. Instead, with a fraction of that budget and a one-person effort, we’ve delivered custom-built, on-demand tools tailored for our business.

The implications are huge: AI enables us to replace multiple subscriptions (email services, social media posting software, chat tools, CRMs, etc.), avoid bulky design teams, and safeguard our IP. And it’s only going to get stronger. Industry-wide, we’re already seeing AI reduce marketing costs, compress design timelines, and streamline repetitive workflows. For brokerages, this means lower overhead, faster responsiveness to clients, and an opportunity to differentiate in a crowded market. If you’re curious about Avery, Sterling, or Pearson—or if you’d like to collaborate—we’d love to connect: info@BluePebbleHomes.com.

Demand: Flat

Supply: Leveling Off

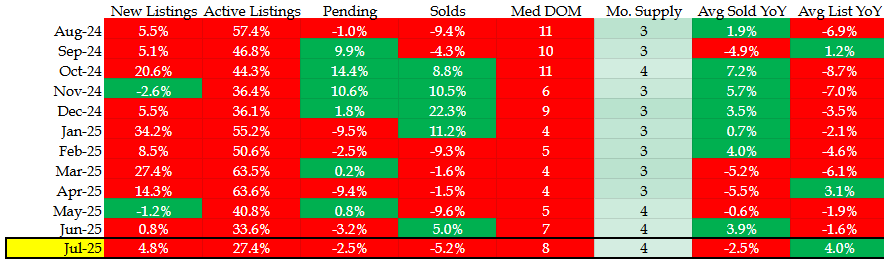

Looking at REColorado data as of August 15, 2025, the Denver metro real estate market feels very similar to last year. Active supply is up slightly, demand is steady, and homes are sitting on the market longer. A 20% year-over-year increase in listings means homes are taking, on average, eight more days to sell than a year ago.

Denver Metro Real Estate Market Data - REColorado, August 2025

Importantly, the shift from a “seller’s market” to a more “neutral” one is recent. May 2025 marked the first time in nearly a decade that supply exceeded three months of inventory—the traditional threshold for when home price appreciation stalls. The last three months confirm the trend: housing prices have essentially flattened. This mirrors national trends where more markets are tipping into neutral territory after years of seller dominance.

Anecdotally, we’re running into more sellers holding price expectations disconnected from the market—say, asking $600,000 when comps point closer to $550,000. As the market shifts and sellers lose leverage, some late-cycle entrants seem eager to cash out or trade up before momentum fades. That’s their right, of course, but here’s our advice: if you *need* to sell, price correctly from the start. It’s far better to take a haircut upfront than to overprice and let your home languish on the market. Buyers today are savvy, and the longer a property sits, the more aggressive they’ll get. If you’re testing the waters, go ahead and shoot high. But if you really need to sell, make sure you’re aligned with the market. Our agents at Blue Pebble Homes are ready to help you determine your home’s true value right now.

---