The Reroute

Back in July, we warned that politicizing the Federal Reserve would backfire. Six months later, the warning is playing out in real time. The dollar has fallen to its lowest level since February 2022. Gold has blown through $5,000 an ounce. And global trade partners are actively restructuring their relationships to reduce exposure to the United States. The market is not panicking, but it is repricing, and that repricing has implications for mortgage rates, home affordability, and the broader economy.

The Skim:

1. The World Reroutes

2. Demand: Softer but Present

3. Supply: Stabilizing

The World Reroutes

The Federal Reserve has been under sustained pressure from the executive branch for over a year. That pressure escalated this month when the Department of Justice opened an investigation into Fed Chair Jerome Powell over the central bank's headquarters renovation project. Powell responded publicly, calling the investigation a "pretext" for political intimidation. It was an extraordinary statement from a sitting Fed chair, and it landed with markets already on edge about who will replace Powell when his term expires in May.

The dollar index has fallen to 96, down nearly 11% over the past year and at its lowest level since February 2022. Gold has surged past $5,000 an ounce, up more than 17% year to date. These moves reflect what analysts have started calling the "Sell America" trade: investors reducing exposure to U.S. assets because of concerns about policy credibility. The irony is hard to miss. The stated goal is lower borrowing costs, but undermining Fed independence is exactly the thing that pushes long-term rates higher.

What has changed since July is that the rest of the world is not just hedging into gold. They are actively restructuring trade relationships. Today, the European Union and India announced a sweeping free trade agreement after nearly two decades of stalled negotiations. European Commission President Ursula von der Leyen called it the "mother of all deals." Indian Prime Minister Narendra Modi said it would "strengthen stability in the international system" at a time of "turmoil in the global order." The timing is not subtle. The deal was announced days after Trump threatened tariffs on eight European countries over their objections to his pursuit of Greenland.

This follows similar EU agreements with Japan, Indonesia, Mexico, and the Mercosur bloc over the past year. Brussels has accelerated its outreach under the banner of "strategic autonomy," which in practice means reducing reliance on a U.S. that European leaders increasingly view as unpredictable. European countries collectively hold around $8 trillion in U.S. bonds and equities, roughly twice as much as the rest of the world combined. If those holders start hedging their exposure or repatriating capital, the math on U.S. borrowing costs changes quickly. The path to sustainably lower mortgage rates runs through institutional credibility, not political pressure.

Demand: Softer but Present

Supply: Stabilizing

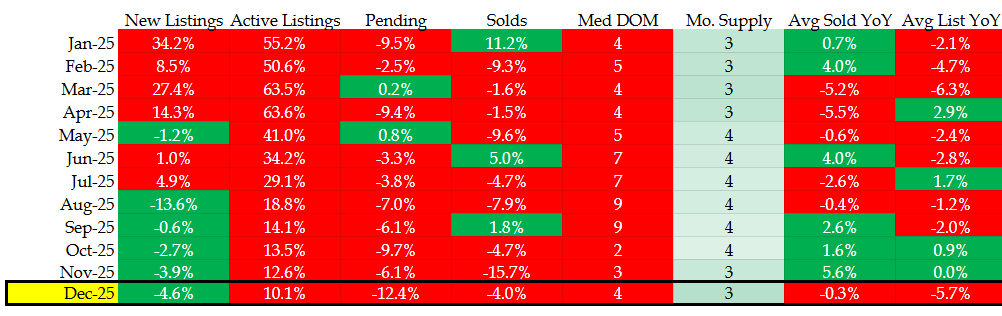

Let's check in on our trusty table summarizing the market conditions around Denver, CO:

Denver Metro Real Estate Market Data - REColorado, January 2026.

Against this macro backdrop, Denver's real estate market is doing something almost refreshing: staying boring. Looking at REColorado data through December, pending activity is softer, down around 12% compared to last year, and homes are sitting a bit longer on market. Median days on market stretched to 39, up from 35 a year ago. But we are still under four months of supply which suggests firm pricing, and that's exactly what we're seeing. While there might be signs of distress in some areas, Denver doesn't appear to be one of them.

On the supply side, active listings are up about 10% year over year, but new listings actually declined slightly in December. This is further eating into the surplus that's been trending down over the last year. The market is definitely more negotiated than it was two or three years ago, and it is functioning normally (just a few days slower than early last year).

Looking Forward

We are constructive on the spring. With supply stabilizing and less than four months of inventory on the market, prices should evolve in a way that it's unlikely to run away from anyone. Buyers will have a good opportunity to start shopping early, with more choices and more negotiating leverage than they have had in years.

For sellers, the calculus is different. The odds are high, especially if you're reaching on price, that it might take you a couple of weeks longer than you'd hope. There is an old adage that your first offer is going to be your best offer, and this market is likely to work that way. If you get a reasonable offer in the first week or two, take it seriously. The longer a property sits, the more aggressive buyers will get on price. So, it's really important to get your house sold quickly or risk becoming a stale listing.