June '26: The Catch-Up

For three months we've been writing about a camel with a loaded back. In March we called it "The Straw" — Iran lit a match next to an economy that was already holding its breath. In April we asked whether the spring was real or a "Lookalike" of last year's fade, and we flagged three slow pipelines — fertilizer into food, jet fuel into diesel, and consumer credit at the bottom of the stack — that were already in motion regardless of any ceasefire headline.

The camel is still standing. The ceasefire that kept expiring and re-escalating through the spring has, for now, held. Energy has come back in. And the single most useful thing we can tell you this month is that the story underneath Denver's spring turned out to be simpler and more hopeful than the macro backdrop would suggest: 2026 came into the year with real momentum, the war put that momentum on pause for about two months, and the market is now working off the backlog. This is a catch-up.

That doesn't mean the national picture is clean. It isn't. But for the first time since January, the local story and the national story are pulling in slightly different directions — and that gap is where the opportunity lives.

The Skim:

1. The Peak That Wasn't the Point — May inflation hit a three-year high, but it's an energy story that's already unwinding. The real news is the Fed flipping from "when do we cut" to "do we hike."

2. Halted, Then Catching Up — Denver came in hot, the war flat-lined new contracts for two months, and closings are now clearing the backlog. Average sold price just hit an all-time high.

3. Two Markets, Still Diverging — Detached is the tightest it's been since 2022. Attached has now closed fewer homes for six straight years. The aggregate "stability" is a coincidence.

---

The Peak That Wasn't the Point

The headline number is ugly, and we want to deal with it honestly before we explain why it matters less than it looks. Headline CPI hit 4.2% in May, the highest annual reading since April 2023 and the third straight month of acceleration: 3.3% in March, 3.8% in April, 4.2% in May. On its face, that's the kind of number that ends housing recoveries.

But look one layer down and the picture inverts. More than 60% of that monthly increase was energy. Gasoline alone was up roughly 40% year over year. Strip out food and energy and core CPI rose just 0.2% for the month and 2.9% for the year — below expectations and *down* from April's pace. The oil shock we wrote about in March did exactly what an oil shock does: it spiked the headline. What it did *not* do, at least not yet, is bleed broadly into the rest of the basket. The thing we feared in "The Straw" — energy pass-through into everything — has so far stayed mostly contained to energy.

And here's the part that matters for anyone thinking about a mortgage: the energy spike is already reversing. Gas prices have fallen sharply since the ceasefire held, and the consensus among the economists we read is that May was very likely the peak for headline inflation this cycle. The April pipelines we flagged are still worth watching — the food and logistics costs work through with a lag, and the May PCE print landing this week is the first real read on whether they're arriving — but the recoverable part of this inflation story, the gasoline part, is recovering.

The real news in June wasn't the CPI print. It was the Fed.

On June 17, in Kevin Warsh's first meeting as Chair, the FOMC held the funds rate at 3.50%–3.75% on a unanimous 12–0 vote. That was expected. What wasn't fully priced was the projections underneath. In March, the median policymaker still pencilled in a rate *cut* for 2026. As of June, that flipped: the median now sees the year ending *higher* than today, and 17 of 18 officials judged the risks to inflation as tilted to the upside, with not a single one seeing downside risk. The committee marked its year-end inflation forecast up to 3.6% and trimmed growth to 2.2%. Warsh, characteristically, declined to offer his own forecast and cut the statement down to 130 words.

Translate that for the rate sheet: the path to lower mortgage rates that we kept squinting for through the winter is gone for now. You don't get to 5% mortgages when the Fed is debating whether its next move is a *hike*. The 30-year fixed has been grinding in the low-to-mid 6s, and the honest base case is that the rate environment you're looking at today is the one you're looking at through the fall. We've said it before and the data keeps re-earning it: plan around the rate you can get, not the rate you're hoping for.

The broader economy, for its part, is doing the stagflation-adjacent thing it's been threatening to do all year. Q1 GDP was revised down to 1.6%. The labor market added a strong-looking 172,000 jobs in May, but the gains were narrow — health care, leisure and hospitality, local government — while financial activities shed workers, and the share of the unemployed who've been out of work for six months or longer climbed to a cycle-high 27.5%. It's the same low-hire, low-fire market we described in April: stable if you have a job, brutal if you're trying to find one. Real wages went slightly negative again in May. The consumer is still spending, but increasingly on the essentials, with the gains concentrated in gas and groceries rather than discretionary.

None of that is good. But notice what it adds up to for housing specifically: rates are stuck, the qualified-and-employed buyer is fine, and the marginal buyer is getting squeezed. Hold that thought, because it's exactly the shape of what's happening in Denver.

---

Halted, Then Catching Up

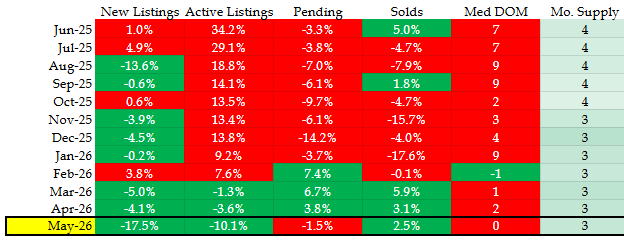

Let's check in on our trusty table summarizing market conditions around the Denver metro:

Here's the shape of Denver's year, and it's worth tracing month by month because the shape *is* the story.

The market came into 2026 with real force. After a genuinely frozen January — 47 days on market, just 794 aggregate closings, the kind of month that looks like distress — contract activity exploded. Aggregate pending sales jumped nearly 31% month-over-month in February and another 26% in March, landing at 1,760 signed contracts. That was the strongest March for new contracts since 2022, up almost 7% year over year. Detached pendings were running double-digits ahead of last year. This was not a lukewarm spring. This was pent-up demand that had been sitting on its hands through a weak fall and a frozen January finally deciding the math worked.

Then it stopped. From the March peak, aggregate pendings rolled over — down 11% in April, then flat into May — and the year-over-year premium that had been sitting at +7% in March decayed to +4% in April and went slightly *negative* by May. Pendings are the leading edge of the market: they're contracts signed *this month*, the cleanest read we have on what buyers are actually doing in real time. And what buyers did, right as the Iran war escalated and the ceasefire kept threatening to fall apart, was pause. Not panic — pause. They stopped signing at the pace they'd been signing.

If the story ended there, we'd be writing a gloomier piece. But it doesn't, because of where the strength shows up instead. While pendings faded, closings kept climbing. Aggregate solds went 1,554 in March to 1,687 in April to 1,671 in May. Detached closings rose every single month — 1,118, then 1,214, then 1,223. That's not a contradiction; it's a lag. Contracts take 30 to 45 days to reach the closing table, so the strong February–March signing wave, plus the contracts that did get written once the ceasefire held, are flowing through to closings *now*. The pendings dip and the solds strength are the two halves of the same sentence: halted in the spring, catching up in the summer.

The headline that falls out of all this is genuinely strong. The average sold price across the metro hit $765,614 in May — an all-time high in our dataset, up 8.2% year over year and above even last June's prior peak. And it got there not on a demand boom but on a supply drought: new listings were down 17.5% year over year and active inventory down 10%, while closings still rose. Fewer homes, roughly steady demand, record prices. That's scarcity doing the pricing work, and it's the cleanest argument we can make that this market has a firm floor under it even with rates stuck in the 6s.

The open question — the one June's data will answer and we'll be writing about next month — is whether pendings *re-accelerate* now that the ceasefire has held. If buyers who paused in April and May come back to the table in June, the catch-up thesis is confirmed and the back half of the summer has real legs. If they don't, then the war didn't pause demand so much as pull it forward, and the spring was the top. We lean toward the former, but we've been doing this long enough to flag the fork rather than pretend we can't see it.

---

Two Markets, Still Diverging

We've been writing for months about the split between detached and attached homes, and we want to put a number on it this month that we think reframes the whole thing.

We pulled year-to-date closings — January through May — for every year back to 2021, and split detached from attached. The detached share of the market has risen *every single year, without exception*: 57% in 2021, then 59%, 62%, 66%, 68%, and now 72% in 2026. This is not a 2026 story or a rate-cycle story. It's a half-decade structural migration, and it is still accelerating.

Underneath that share number are two completely different markets.

Detached is the bright spot, and it's not close. Months of supply sit at 2.1. Median days on market is eight. The average detached home sold for $875,000 in May, an all-time high, and the price has been climbing hard all spring — up nearly 9% in March alone. Year-to-date detached closings of 4,911 are the highest since 2022 and up 5% over last year. This is a tight, fast, functioning, competitive market, and it's the engine carrying the entire metro's numbers. If you own a detached home that shows well and you price it correctly, the next sixty days are your window — buyers are competing and inventory is scarce.

Attached is the opposite story, and it's been the opposite story for years. Months of supply sit at 5.9 — nearly three times the detached figure. Days on market is 30. And the volume trend is the one that should stop you: year-to-date attached closings have fallen for six straight years — 4,527 in 2021 down to 1,932 in 2026. The for-sale condo and townhome market in Denver Proper is now less than half the size it was at the start of the decade, and it fell another 11% just this year. Average attached price is technically up, but on a thin and shrinking base we'd read that number with caution.

This is the macro thesis from the first section reaching Denver, precisely where we predicted it would. The core attached buyer is the first-time buyer — the exact cohort getting squeezed by stuck rates, negative real wages, and a grocery bill that keeps climbing. And their alternative to buying isn't buying; it's renting one of the many new, amenitized luxury apartment buildings that have flooded the metro, often for less per month in real terms than owning. Every month rates stay high and the rental glut keeps absorbing, the math to own an attached unit gets worse while the math to own a detached home gets better for an entirely different, more insulated buyer.

The aggregate market looks "stable" this year — 6,843 closings year-to-date, essentially dead even with 2025. But that stability is a coincidence. It's detached recovery just barely outrunning attached collapse, two violently diverging trends that happen to net to flat. Strip them apart and nothing about this market is stable. It's two markets moving in opposite directions.

---

Looking Forward

We titled the last three pieces around a camel with too much on its back. The camel is still walking. The ceasefire held, inflation likely peaked, and Denver's spring — once you trace the monthly shape — turns out to have been a pent-up demand story interrupted by a war and now catching up, rather than another lookalike fade. That's a better outcome than the April setup had any right to produce.

But "better than feared" is not "all clear." Rates are stuck, the Fed is openly weighing a hike, the food and logistics pipelines we flagged in April are still landing on a lag, and the bottom of the consumer stack is still under real pressure. The single variable most worth watching for the rest of the year is still the grocery bill, not the funds rate — and locally, it's whether June pendings come back.

For buyers: Rates aren't improving soon, so stop waiting on them. The real opportunity right now is segment-specific. If you're shopping detached, inventory is genuinely scarce and competition is real — be ready to move on the right home. If you're shopping attached, you have leverage you haven't had in years; the buyer pool is thin and getting thinner, so use it.

For detached sellers: This is your window. Tight supply, record prices, eight days on market. Price it right and let the market reward you. Don't get greedy chasing the all-time-high headline — the buyers showing up are qualified and disciplined, not desperate.

For attached sellers: Be honest about what you're competing with. It's not just the other condos on your street; it's every luxury apartment that opened in the last three years. Price it to move, because the pool of buyers for your unit is structurally shrinking, not cyclically dipping.

And the advice from every month this year still holds: stay patient, stay realistic, and don't trust anyone — including us — who tells you they know exactly how this ends. We'll have June's pendings next month, and that's the number that tells us whether the catch-up has legs.

Tags

Denver housing market · Colorado real estate · mortgage rates 2026 · Federal Reserve · Inflation