March 2026 Market Insights: The Straw

The economy was already holding its breath. Now it's holding a match.

For the past year, we've been threading a needle most people didn't know existed: coming out of inflation, searching for the Goldilocks rate that's not too hot, not too cold. Inflation was trending in the right direction. The consumer was slowing but not collapsing. The labor market was softening — gently. The path to lower mortgage rates was there, if you squinted: get CPI at or below 2%, let the Fed ease short-term rates enough that the 10-year follows. That path is now on fire.

The Skim:

- The Tinderbox — Policy friction and Iran have repriced inflation risk at the worst possible moment

- Demand — The Reset Worked! — Pending activity up 10% YoY as buyers respond to January's price correction

- Supply — Detached > Attached (Again) — Single-family moving in days; condos stuck competing with rental glut

The Tinderbox

Before Iran, the administration had already been stacking inflationary pressure onto an economy that didn't need more of it.

Tariffs are the obvious one. The Supreme Court struck down IEEPA tariffs in February — executive overreach, they called it. The market exhaled for a week. Then Section 301 investigations launched against sixteen trading partners: China, Mexico, the EU, sixty-odd other countries. The tariff pressure isn't going away; it's finding a new legal wrapper. The threat alone adds uncertainty. Actual implementation adds direct cost-push inflation on everything from electronics to auto parts.

Deportations are the quieter pressure. Remove workers from construction, agriculture, and services, and you don't fix inflation — you feed it. Fewer workers means higher wages to attract the ones who remain, which means higher costs, which means higher prices. The construction industry was already short on labor; removing workers now makes every home more expensive to build.

Fed pressure is the most ironic. The stated goal is lower rates. The actual effect is the opposite. When the executive branch campaigns to remove the Fed chair, when the DOJ investigates central bank leadership, the bond market notices. Long-term rates don't fall when institutional credibility is under attack — they rise. The 10-year yield is set by investors pricing risk, and that risk now includes "what happens when the adults leave the room?" Gold above $5,100. Dollar at its lowest since February 2022. The market is saying: we're not sure we trust this anymore.

Then Iran hit — not just an oil shock, but a supply-chain bomb with a long fuse. Oil spiked 10-13% in the first week, with Goldman calling for $100+ if it drags on. But the deeper problem is long-term inflation expectations. China depends on Iranian oil. When that supply gets repriced, production costs rise in Shenzhen, shipping costs rise on container routes, prices rise at Target six months later. The February CPI of 2.4%? Economists are already calling it outdated. The real inflation story is being written in procurement offices, not government spreadsheets.

The timing couldn't be worse. February's jobs report came in at -92,000 — one of the largest declines since the pandemic. Unemployment ticked to 4.44%, highest since late 2021. Consumer sentiment is taking a direct hit just as the labor market cracks. The risk is a squeeze from both ends: inflation expectations rising while spending and employment soften. That's not stagflation yet — but it's stagflation's area code.

The Fed meets this week with 99% odds of doing nothing. Cut rates and risk reigniting inflation. Hold rates and watch employment deteriorate. That's not confidence — that's paralysis.

What this means for rates: The 30-year fixed is back above 6% and climbing. You don't get to 5% mortgages by pressuring the Fed on Twitter. You get there by convincing bond investors that inflation is controlled and policy is predictable. We're doing the opposite on both fronts. For buyers, the rate environment you see today is probably the one you'll see for six months. Plan accordingly.

Demand: The Reset Worked!

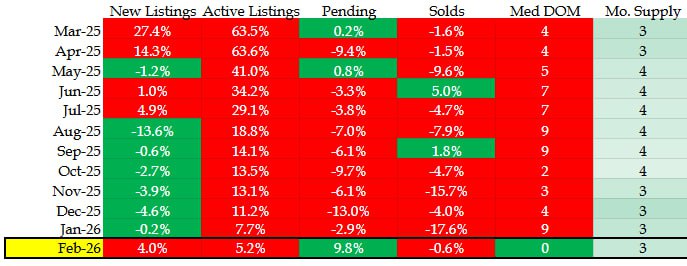

Let's check in on our trusty table summarizing market conditions around the Denver metro:

In January, the market felt frozen. Median days on market stretched to 47 — nearly seven weeks to sell a home. Sold activity cratered to 794 units, down 17.6% YoY. Pending dropped to 1,077. Buyer momentum didn't slow; it evaporated.

But underneath the surface, prices reset. Average sold price down 6% YoY in January — a meaningful correction that finally found a level buyers could clear.

By February, they noticed. Pending activity jumped to 1,430 contracts — up 9.8% YoY, the strongest reading in months. Solds recovered to 1,131. And the headline number: days on market collapsed from 47 to 24. The market went from frozen to functional in four weeks.

New listings ticked up to 2,088 (+4% YoY), suggesting sellers are gaining confidence. Active inventory at 3,942 with three months of supply — balanced, not bloated.

The January price correction worked. Buyers who'd been sitting on the sidelines finally saw value and moved. The market isn't roaring — let's not get ahead of ourselves — but it's waking up earlier than 2025. For buyers who've been patient: the window to negotiate hard on price may be narrowing.

Supply: Detached > Attached (Again)

February tells two very different stories depending on what you're buying.

Single-family detached is back. Days on market below 30 again. Well-priced homes in good condition transacting in a weekend — some with multiple offers, some with bidding wars. The buyers who've reset expectations on rates are competing for limited, quality inventory. If you're a seller with a detached home that shows well and prices correctly, this is your market.

Attached product is stuck. Many condo sellers still haven't adjusted to how much demand has shifted. Part of it is rates hitting first-time buyers hardest — that's the core condo demographic. But the bigger issue is competition: Denver has delivered enormous luxury rental inventory in recent years. Those buildings are nice, amenitized, professionally managed. And they're competing directly with for-sale condos.

The math is simple: why buy a 15-year-old condo with a $400 HOA and a 6.5% mortgage when you can rent a new apartment with a pool and gym for $2,200 a month? Until rental rates firm up — signaling the glut is absorbed — it's hard for us to get bullish on attached product.

If you're selling a condo, price it to move. Your competition isn't just other condos for sale; it's every luxury apartment that opened in the last three years. If you're buying one, you have leverage — use it.

Looking Forward

The national picture is uncertain — maybe more than since the pandemic's early days. Tariffs, war, a paralyzed Fed, an economy running out of cushion. We titled this "The Straw" for a reason: the camel's back was already loaded. Iran might be what tips it over.

But locally, Denver shows signs of life earlier than expected. The January price reset worked. February pending numbers confirm buyers are responding. Single-family is moving. Attached is struggling. Spring is starting.

For buyers: Rates aren't changing soon, but competitive dynamics might. If you're qualified and ready, act before inventory tightens further.

For sellers: Single-family in great condition moves fast. Everything else requires realistic pricing. The market rewards honesty with yourself.

Stay cautious. Stay patient. And don't believe anyone who tells you they know how this ends.