October '25: Currency of Confidence

With October underway, the mood in the markets feels tense but oddly quiet — like everyone's waiting for a signal that still hasn't arrived. The federal shutdown has frozen key economic data, leaving traders, analysts, and policymakers flying blind at a time when confidence is already fragile. Gold has become the proxy for that uncertainty, breaking through $4,200 and reminding everyone that faith in fiat currencies — and in fiscal discipline — has limits. It's a strange backdrop for markets that are normally information-obsessed. Without fresh CPI, NFP, or GDP to trade on, the conversation has shifted from analysis to narrative — and the narrative is starting to fracture.

Back here at home, Denver's real estate market is doing something refreshing in contrast: staying on trend. After a slow August, September brought a small bounce and a return to normal rhythm — not exuberant, not panicked, just steady. In a month where global markets are questioning value itself, local housing has found some.

---

Gold: The Currency of Confidence

There's something unusual happening in the markets right now, and it's not hiding in the inflation data or the job numbers — mostly because those numbers haven't been published. The federal shutdown has effectively blinded investors to the most critical indicators of economic health: job growth, wage gains, and price stability. Without those datapoints, the entire macro conversation is running on instinct, sentiment, and narrative. And lately, that narrative has been flashing gold.

Spot gold price chart over the last year (TradingView).

Gold prices have gone vertical — from the $2,600s early this year to north of $4,200 today — a breathtaking move that can't be explained by short-term rate speculation alone. Part of it is mechanical: with key economic releases frozen and Washington locked in gridlock, traders have defaulted to the one signal that never stops printing — fear. But beneath that fear sits something deeper: a growing recognition that the long-term fiscal math just doesn't work. Central banks are buying gold at the fastest pace in decades, not because they're panicking, but because they're hedging. When central banks start treating their own reserves as a liability, everyone else pays attention.

This isn't new — the World Gold Council has been documenting record central-bank purchases for the past three years — but the timing of this latest acceleration matters. When the official data goes dark, markets start writing their own story. ADP's recent private payroll report hinted at job losses, inflation trackers are edging higher again, and whispers of renewed U.S.–China trade tension are rekindling the specter of 2019-style tariff inflation. Add to that a few cracks in regional bank balance sheets and a muted but real slowdown in consumer discretionary spending, and you've got the ingredients for a crisis of confidence — not in the economy itself, but in what the numbers actually mean and who's equipped to respond.

What's remarkable is how synchronized these pressures have become. A softening labor market points toward rate cuts, but sticky inflation and fiscal strain make those cuts harder to deliver. Every path forward seems to lead to the same conclusion: money is losing a little bit of its meaning. Whether that loss of faith is justified or premature, it's showing up in real time — in gold, in widening credit spreads, and in the tone of market commentary that's quietly shifting from cautious optimism to resigned uncertainty.

For now, the absence of official data is ironically providing calm; without new numbers to trade on, volatility has stayed muted. But make no mistake — the minute those reports resume, we'll find out whether this gold surge was a warning shot or a confirmation.

As for housing and local markets, the story remains refreshingly boring by comparison: *on trend.* Supply and demand are still tracking close to seasonal norms, pricing is stable, and buyers are adapting to the higher-rate environment with a degree of patience we didn't see a year ago. While Washington debates the debt ceiling and central banks debate the value of their own reserves, Denver's market is quietly doing what it should — finding balance.

---

Demand: Still on Trend

Supply: The New Competition

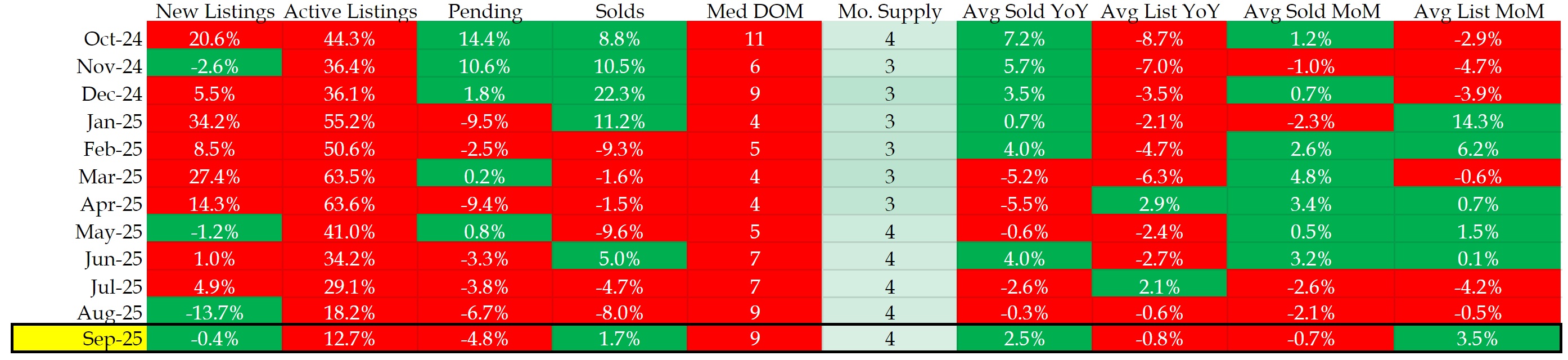

Let's check in on our trusty table summarizing market conditions around the Denver metro market last month:

Denver Metro Real Estate Market Data - REColorado, October 2025.

After a quiet August, September felt like a small but noticeable return to normal rhythm. New listings were essentially flat year-over-year (-0.4%), pending sales slipped -4.8%, and sold volume ticked up +1.7%. None of that screams "breakout," but it does suggest the market has regained its footing after a late-summer lull. The August slowdown — marked by a double-digit drop in new listings — now looks like a brief pause ahead of a larger macro inflection, rather than a sign of real dysfunction.

Still, even though supply is only about 14% higher than it was a year ago, homes are sitting longer. Median days on market have stretched to nine, roughly 8–10 days slower than last year's pace despite a much smaller supply bump. That mismatch says a lot about buyer psychology right now. Where last year's flood of new inventory (50–60% increases in active listings) barely dented momentum, this year's modest rise has had a much larger impact — a sign of consumer fatigue more than a structural imbalance in housing supply.

The reasons aren't mysterious. Inflation hasn't meaningfully cooled, job security is wobbling, and rates — though down from their summer highs — remain elevated enough to squeeze budgets. We even had our first client in years lose a pending purchase because they lost their job midway through closing, something we hadn't seen since 2020. That combination of softer confidence and higher costs explains why buyers are slower to act and quicker to hesitate.

On the supply side, new construction is proving to be both a blessing and a headwind. Builders are still delivering a steady pipeline of smaller, more efficient homes, often with attractive financing incentives that resale sellers simply can't match. In some submarkets, new builds are effectively setting the ceiling for what buyers are willing to pay — not because they're cheaper, but because they're newer, better aligned with current preferences, and easier to finance.

That dynamic is subtly reshaping the resale landscape. Many resale listings — particularly those needing updates or priced too close to new-construction comps — are sitting longer, even when priced reasonably. The market isn't broken; it's just more selective. Buyers are taking their time, comparing incentives, and thinking pragmatically about where they get the best overall value for their payment.

---

The Takeaway

The best word for Denver's housing market right now might be "measured." It's not weak, but it's certainly not racing ahead either. September's data lines up neatly with the broader macro theme of fatigue and recalibration: consumers are still active, but they're cautious. Sellers are adjusting, buyers are negotiating, and homes are finding their level.

In short, the market is on trend — just a slower trend. With the Fed likely to pivot toward easing in the months ahead and long-term rates already inching down, this plateau could set the stage for a more stable winter market than we've seen in several years.