Holding Our Breath

With school back in full swing and adults settling back into normal routines, we are officially back to work and beginning the sprint toward the holidays. This is also the time when senior risk managers return from their summer escapes in the Hamptons to reassess positions and prepare for the macro moves that often hit in September and October.

All of this coincides with a Fed meeting this week that is very likely to move the needle. President Trump has been outspoken about wanting lower rates (and really, what real estate guy does not?), but so far Chairman Powell and the Fed governors have resisted. Now, with data showing a much weaker job market, it seems the Fed may finally be ready to act. The challenge: inflation is still here — and even showing signs of reaccelerating. *So, what happens next?*

---

Waiting for the Fed

This Wednesday (Sept. 17) marks one of the most anticipated Fed meetings in months. The recent softness in the labor market is forcing policymakers to scrutinize employment statistics, and the numbers have been pretty ugly. A few highlights:

- Jobs: Nonfarm payrolls (NFP) in August showed a meager gain of just 22,000 jobs — one of the lowest monthly readings in the last year. On top of that, the Bureau of Labor Statistics (BLS) recently revised down job gains by 911,000 over the 12 months ending in March 2025.

- Wages: After running at 4%+ year-over-year growth coming out of COVID, wage gains are cooling. The most recent BLS release in early September showed wage growth slowing to 3.7% YoY. With fewer jobs being added, employers are under less pressure to boost pay.

- Inflation: Slower wage growth would not be as concerning if inflation were not still persistent. But core inflation ~3.1% YoY means *real* wage growth — the purchasing power of workers — is declining. As buying power slips, it becomes harder to sustain the consumer spending that drove much of the post-pandemic expansion.

Taken together, these trends show consumers are facing a double hit: a softer labor market with longer unemployment durations, plus inflation that refuses to cooperate.

That leaves the Fed in a tough spot. They have already acknowledged labor-market weakness as a growing concern, and that is why markets widely expect a rate cut this week. But the bigger focus will not just be the decision itself — it will be Powell is comments about how the Fed plans to balance inflation vs. jobs, and what the future path of rates might look like.

Our call: We expect the Fed to cut rates, but the reaction may be mixed. Inflation is still sticky, and tariff-related pressures add uncertainty. A short-term cut could boost hiring and investment, but it also risks fueling long-term inflation expectations. That means short-term rates may come down while 10–30 year yields push higher. The Fed is unlikely to commit to aggressive future cuts until it sees clearer progress toward its 2% goal.

---

Demand: On-Trend

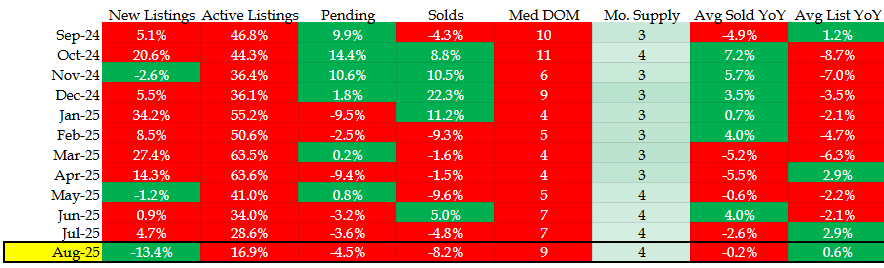

Let us turn to the local real estate market and take a look at our trusty data table summarizing activity in the Denver metro area:

Denver Metro Real Estate Market Data - REColorado, September 2025

Long-term interest rates have drifted lower by about 0.25% in recent weeks on expectations of a Fed cut. That has been enough to bring some buyers back into the market. Pending activity at the end of August is right on trend with 2024 levels, showing that buyers are gradually adjusting to today is higher-rate environment — a positive sign.

We did see a dip in closed units in August, likely the result of sellers holding out for higher prices before facing seasonal reality. In July, the average list price was up 2.9% while the average sold price fell 2.5%. That 5.4% spread shrank to 1.5% by the end of August, which should support slightly stronger demand heading into fall.

---

Supply: Plateauing

On the supply side, August 2025 brought the first double-digit decline in new listings YoY since September 2023. Between then and now, active supply within 10 miles of downtown Denver had surged 83%, consistently posting 10–30% YoY increases for many months.

The good news is that the recent decline in new listings may start to ease the pricing and absorption pressure we have seen. Since September 2023, median Days on Market (DOM) jumped from 11 to 28, and inventory climbed from 2 months to 4 months. While that means homes are not selling overnight anymore, this level of supply is actually constructive. Prices look stable, and buyers have the luxury of time to shop and negotiate.

That shift also makes real-estate brokers relevant again — which we welcome. Sellers can not just throw a number out and expect an immediate sale, and buyers now benefit from inspections, diligence, and stronger negotiations, just like the pre-2020 market. For many clients, this is a healthier environment.

---

Final Thoughts

While no one knows exactly what the Fed will do this week, we do know this: the Denver market is showing signs of balance. Buyers are adjusting, sellers are moderating expectations, and supply may be reaching a plateau.

Thinking about buying or selling? The combination of more negotiating room, stable prices, and the potential for lower rates could make this an attractive time to act. Reach out — we would love to help. And do not forget to ask about our loan program, which may save you money each month.