Blue Pebble Market Insights - November 2022

OMG. They Killed Kenny!

The Skim:

1) 2023 is Going to be a Doozy

2) Demand Evaporating with Higher Rates

3) Supply Dripping on to the Market

The Federal Reserve is on a conquest to quash inflation, and the effects of their campaign are coming to the surface. As it relates to Denver residential real estate, higher interest rates are leading to an increase in days that homes are “on the market” before going under contract. Bidding wars are much fewer and further between due to the psychology of the market being materially different than it was a few months ago; sellers are finally willing to accept that home values are starting to go down and buyers can barely contain their excitement to negotiate. With everything seeming a little better over the last few weeks due to consolidation in mortgage rates, we need to urge caution. We are preparing for a 10-15% drop in housing prices to start 2023 led by the national homebuilders, and we want our readers to be informed on what's about to happen.

2023 is Going to be a Doozy

Got your attention with that intro, huh? We've seen some extremely interesting anecdotal data coming from a variety of sources throughout the residential market suggesting that the really tough times are ahead. Based on our information, we think the market is going to start to see these changes in the next 60-90 days.

Publicly, homebuilders are ringing alarm bells about what happening in their sales trailers. Here is an article that highlights a steep drop in housing starts only expected to get worse (remember, 2022 included half the year when sales were still hot). Due to uncertainty in market conditions, DR Horton declined to provide forward-looking guidance on sales as part of their recent earnings call which is extremely suspicious. And if you’re not convinced the market is slowing down, here is an article about mortgage applications basically stopping; applying for a mortgage is a prerequisite for most buyers, so the conclusion from this article confirms that the buyer pool is materially smaller now.

Given the above, the following discussion is an argument based on market participant incentives and other market conventions that will lead to an avalanche of supply hitting the market after the first of the year. While that supply might be “available” right now, it’s so overpriced and uncompetitive that it's not selling, so massive price reductions about to be published will bring even more supply to current clearing prices. We believe these changes will lead to general price declines across the Front Range housing market on the order of 10-15%.

Right now, public homebuilders are RACING to close as much of their backlog as possible before the end of the year. The big homebuilders sold a huge amount of lots from 2020 through the first half of 2022, and since then, their sales paces have stalled. When you're a director at a publicly traded homebuilder, you are paid based on earnings and share prices which only get booked when you close homes. Therefore, if you *know* that your sales are slowing substantially and you won't be closing as many homes next year, then you are going to do everything in your power to jam through as many closings as possible this year to pad your numbers. It follows that homebuilders are *extremely* focused right now on closing backlog through the end of the year and are doing everything in their power to protect those closings.

The focus on closing the backlog is forcing builders to keep their advertised prices at the same levels as they've been for the last year or two. If they were to drop prices to be more competitive and find a consistent sales pace, then they would destroy the comps for their pending closings and sacrifice their earnings without any benefit explains why their sales paces have slowed even more than expected.

We have to keep in mind that homebuilders are not private equity firms and do not get paid by their shareholders to take risks on the capital appreciation of their holdings. Instead, builders get paid to sell homes and that requires them to find a consistent sale pace in any market condition, and getting back to something consistent will become the builders' *primary* goal after their incentive structures reset. From an investor's perspective, there is no point in holding stock in a homebuilder that won't sell homes in the future, so the builders' business models will be forced to adapt to satisfy investors very quickly. Capital will go to those builders who are able to demonstrate restarting sales most quickly, so there are incentivizes to rip the band-aid off as quickly as possible until consistent sales can be established.

When the builders start dropping prices in January, it's going to have cascading effects. First, their supply is not competitive in the resale market at current prices, so bringing lowering prices will cause the resale market to slow down even further; it will seem as if more listings magically appeared in the market. Additionally, demonstrably lower sales prices will cause banking issues as financial institutions will be unable to ignore markdowns on land and real estate holdings when it's publicly reported that prices are declining substantially. This will create further slowdowns in investment and some short-term pain for smaller, poorly capitalized builders. Plus, there is a bigger knock-on effect from wealth generation due to housing than the stock market, so broad housing declines will officially start the recession in the US. And from there, we will have to see where things go...

There are three major takeaways from the conversations & data that have led us to these conclusions:

1) Market participants are not talking about massive price reductions because it will jeopardize 2022 financial performance. Everyone is incentivized to behave that way right now, and everyone will share the same incentive to switch tones very quickly.

2) Builders will have to aggressively cut prices on all active homes both completed and under construction. There might be some really, really good opportunities for people looking to buy homes to pick up some of these “distressed” deals as builders offload products in 90-120 days. It also seems they might hold back unsold lots for when they reintroduce new products after the reset, so there this might be a transient opportunity to get a good deal from them at current finish levels.

3) If you need to sell a home, you need to price it aggressively *NOW* and it needs to go under contract before December. Depending on how aggressively the builders will be when they lower prices, I would be concerned about some buyers getting cold feet if you own a home that is being sold in an area competing against new construction after the first of the year.

Demand Evaporating with Higher Rates

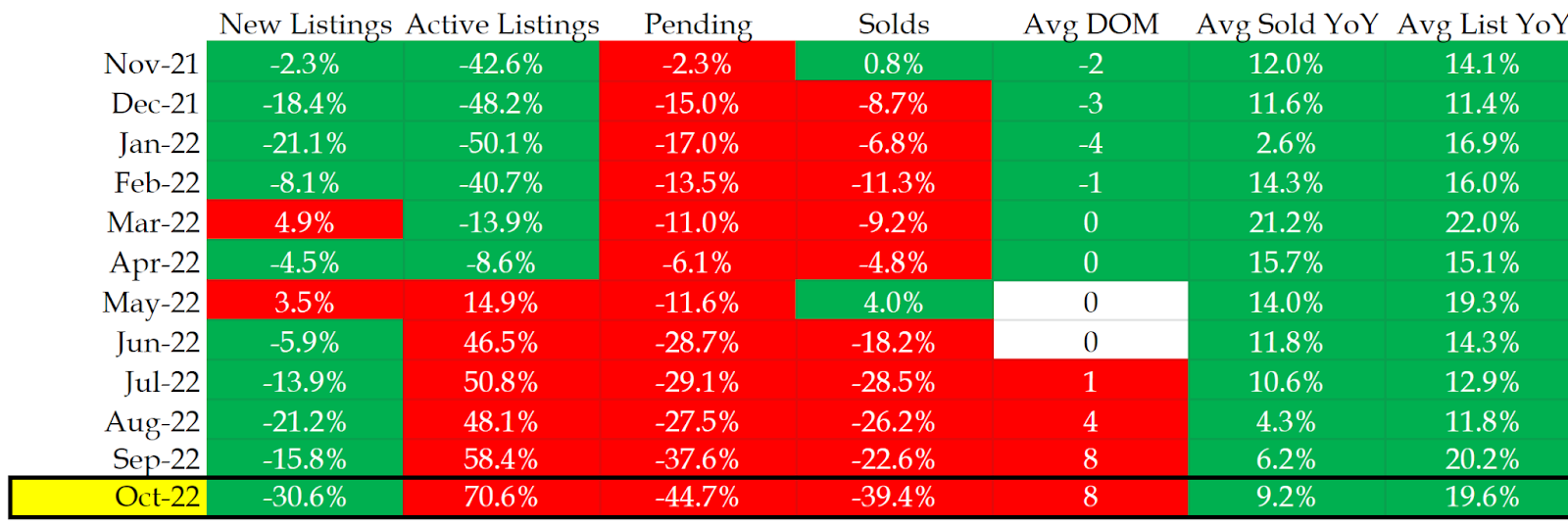

Let’s check our trusty table summarizing real estate market activity in the Denver metro area surrounded by a circle with a 10-mile radius around Union Station:

All Data taken from REColorado between Nov. 10-15, 2022

If you still think we’re in the same market environment as 2021 and the first half of 2022, you are sorely mistaken. There is a very clear shift in trend from April to May of this year that continues to accelerate.

1) New Listings – Down year-over-year with details discussed further in the next section;

2) Active Listings – As of the end of last month, there were 70% more units on the market this year vs. the same period last year. The increase in supply is driven by a slowdown in demand vs. an increase in the pace of new supply;

3) Pending – 50% fewer homes are going under contract now vs. the same time last year. You are seeing price reductions more frequently which gives more evidence of a demand-based slowdown;

4) Sold – Closing activity continues to follow pending activity and we expect next month will reflect an even larger decline than we saw this month. Lower sales paces are consistent with what we’re hearing in the homebuilding space. Since the MLS is primarily resale and can react to prices more quickly into year-end, we have to assume the situation with the builder community is worse.

5) Days on Market (DOM) – This is the most constructive of our indicators as it suggests a slowdown but not yet market conditions that would necessitate a breakdown in prices. The relative strength of this indicator is more a function of year-end motivations vs. a true reflection of what’s happening in the market. “We need to buy/sell before Christmas!” in an environment without a lot of supply. It will be interesting to see how this metric changes in January – it’s where we’d expect the biggest jump when the builders lower prices.

There is a slight reprieve in rates as the market digests higher probabilities of economic slowdowns in the last two weeks. That has led to a small spike in showings and activity before the end of the year, but we really need to keep this in context for the wave we expect to hit in 2023.

Supply Dripping on to the Market

In the absence of an economic depression accompanied by spiking unemployment, we expect supply to stay structurally lower for at least a generation. Yes, supply will be lower for at least 15-20 years (if it ever recovers to pre-pandemic levels). The market would need a “spike” in unemployment vs. just a recession to get a whole generation of homeowners who locked in monthly mortgage payments are historic low rates to monetize the equity in their homes and reset into a higher mortgage or rental situation.

As a result, here’s what is happening to supply metrics:

6) New Listings – For the reasons mentioned above re: the cost of homes and financing, new listings will hit the market more slowly for a long, long time. This will likely only start to change when unemployment goes above 7.5% nationally;

7) Avg Sold vs. List Prices – The huge spread between list and sale prices last month came down a bit driven by negotiations where buyers didn’t quite get the lowball offers they wanted. Sellers know that supply is still relatively low, so they are sticking to their guns for now. We expect prices to be under pressure at the start of the year when the builders get more competitive.

It’s also a helpful comparison to check where we are versus 2019 to show how much the market has changed in the last few years. Below is an output of our table if we used the comparison from Oct 2019 against the metrics from last month:

A comparison of the market at the end of Oct ‘22 vs. Oct ‘19 — very different. Data from REColorado.

Supply is down 80% now versus 2019 while pace now is only down 10%. With new listings now down 18%, we are seeing a more “balanced” market, a market which is still extremely tight as there is not much supply should the market start to pick back up again.

This is likely the reason why things are so confusing right now: there is no supply and no demand. What happens when everything stops for a few months? I guess we’re going to find out.